.jpg)

How Dental Insurance Deductibles and Co-Pays Affect Dental Practices

For dental teams, understanding insurance terms like deductibles, co-pays, and coinsurance is critical. These components directly influence patient billing, claim processing, and revenue cycle management. Misunderstandings or miscalculations can cause delayed payments, billing disputes, or under-collection, impacting the practice’s financial health.

Front desk staff and billing teams often spend significant time explaining patient costs while ensuring claims are processed accurately. Clear knowledge of cost-sharing elements allows practices to streamline reimbursement, improve collections, and maintain predictable cash flow.

This guide explains these terms from a practice management perspective and provides actionable strategies for optimizing insurance reimbursement.

Key Takeaways

-

Deductibles determine when insurance reimbursement begins. Dental practices must verify deductible status in advance to estimate patient responsibility and prevent billing surprises.

-

Co-pays and coinsurance define the patient’s cost share. Understanding these amounts helps front desk and billing teams communicate accurate financial expectations before treatment.

-

Clear verification and explanation of benefits improve collections. When dental teams understand how deductibles, co-pays, and coverage limits interact, they can reduce disputes and streamline the dental insurance claims process.

Deductibles and Co-Pays: Two Cost-Sharing Elements Dental Practices Must Understand

In dental insurance billing, deductibles and co-pays are two of the most common cost-sharing components that directly affect treatment estimates, claim submissions, and patient collections. For dental practices, understanding how these two elements work is essential for setting accurate financial expectations and avoiding reimbursement complications.

A deductible represents the amount a patient must pay out-of-pocket before the dental insurance plan begins contributing toward covered procedures. A co-pay, on the other hand, is a predetermined fee the patient pays at the time of certain visits or treatments, regardless of the total service cost.

Deductible vs. Co-Pay: When Each Applies

For dental billing teams, the key difference lies in when these payments occur during the insurance process.

-

Deductibles act as the initial financial threshold before insurance participation begins.

-

Co-pays are fixed payments typically collected at the time of service.

-

Both influence treatment planning estimates, claim reimbursement calculations, and patient financial responsibility.

When dental practices verify benefits and document these cost-sharing elements correctly, they can reduce billing disputes, improve patient transparency, and process dental insurance claims more efficiently.

What Does a Dental Co-Pay Actually Cover?

A dental co-pay, commonly written as a co-payment, is a fixed amount assigned by an insurance plan for specific visits or services. Because the amount is predetermined, it becomes one of the easiest portions of patient responsibility to estimate and collect during the appointment.

In many dental plans, co-pays are associated with routine or preventive services and remain consistent regardless of the total procedure fee. For example, a plan may require a $20 co-pay for an exam or preventive visit, even if additional services such as fluoride treatment are included during the appointment.

From a billing and insurance verification standpoint, co-pays typically apply to services such as:

-

Routine dental examinations

-

Preventive cleanings

-

Diagnostic consultations or evaluations

It is important to note that co-pays do not replace deductibles. Even after a patient has met the deductible requirement for the year, the insurance plan may still assign a co-pay for certain visits. Because of this, co-pays remain a consistent component of patient responsibility that must be communicated clearly during treatment planning and financial discussions.

The Importance of Deductibles in Dental Insurance

A deductible represents the initial portion of treatment costs that the patient must cover before the insurance carrier begins sharing expenses. Unlike co-pays, which apply to individual visits, the deductible accumulates over time until the required annual amount has been satisfied.

For example, consider a dental plan with a $500 deductible. If a crown procedure costs $600, the first $500 is typically applied toward the deductible. After this threshold is reached, the insurance plan begins contributing to the remaining treatment cost based on the coverage structure defined in the policy.

Once the deductible is met, insurance participation generally applies to other covered procedures within the same benefit year. Deductibles, therefore, play a significant role when planning or estimating restorative and major treatments, including:

-

Fillings

-

Extractions

-

Root canal therapy

-

Crowns or other restorative procedures

Preventive services are often structured differently. Many dental insurance plans cover exams, cleanings, and basic diagnostics without requiring the deductible to be met first, which encourages regular preventive care while helping control long-term treatment costs.

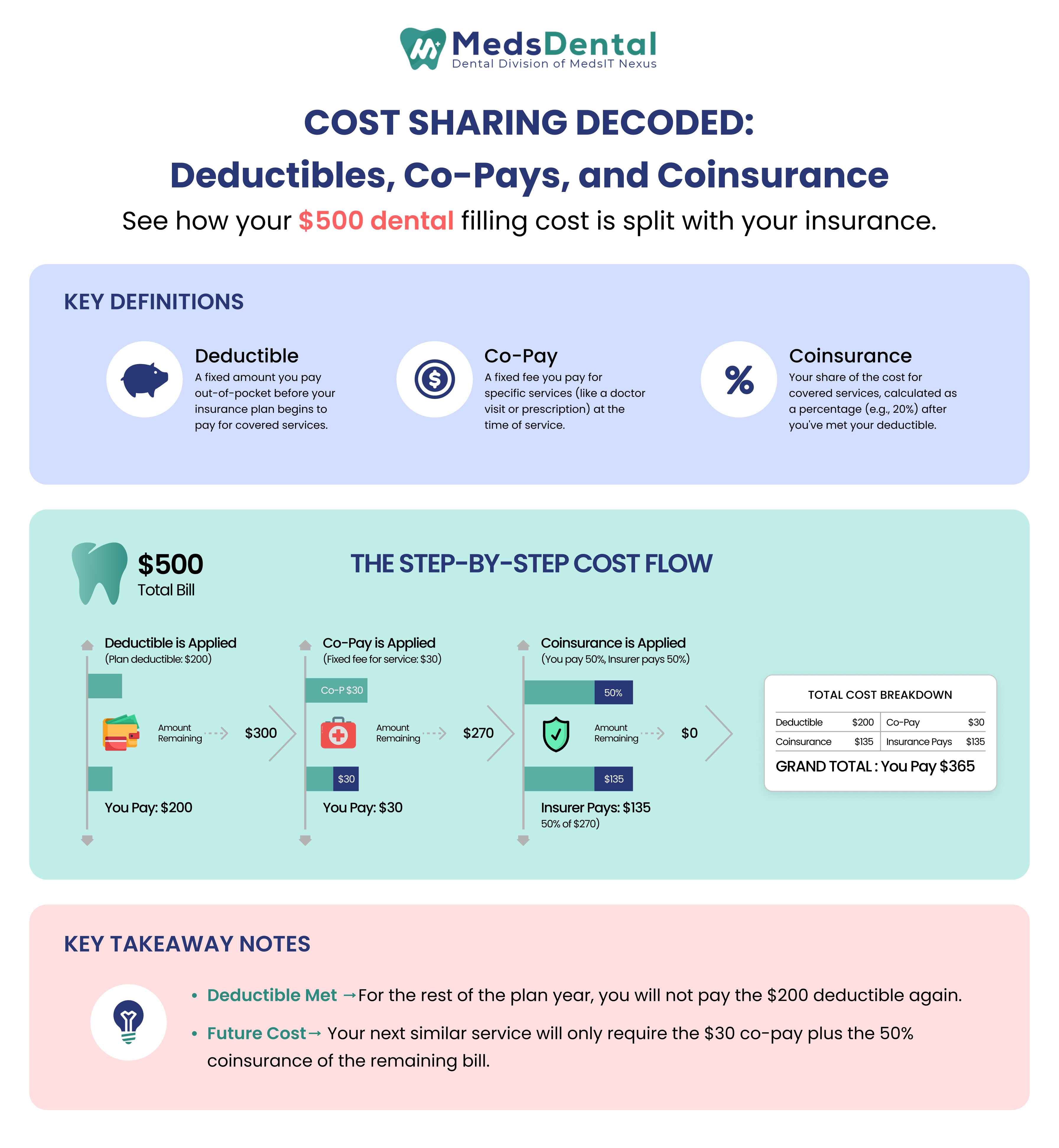

Cost Sharing Explained: Coinsurance vs. Co-Pays vs Deductibles

Understanding how coinsurance, co-pays, and deductibles interact is critical for accurately estimating patient responsibility and managing reimbursements efficiently. Each component influences billing, claims submission, and cash flow, making it essential for front desk and billing teams to calculate totals before treatment.

How These Components Work Together

Consider a scenario where a patient needs a $500 dental filling under a typical insurance plan:

-

Deductible: The first $200 goes toward the annual deductible. This amount must be collected from the patient before insurance contributions apply.

-

Co-Pay: After the deductible is met, the plan may require a $30 co-pay for the visit. This fee is typically collected at the time of service.

-

Coinsurance: The remaining balance ($500 − $200 deductible = $300) is shared between the insurer and patient based on coinsurance. If the coinsurance is 50%, the patient pays $150, and the insurer covers the other half.

Total patient responsibility:

-

Deductible: $200

-

Co-Pay: $30

-

Coinsurance (50% of $300): $150

-

Grand Total: $380

This approach helps billing teams provide clear cost estimates, prevent payment delays, and improve insurance claim accuracy.

Why Providers Should Track These Components

-

Treatment Planning: Accurate calculation of co-pays, deductibles, and coinsurance ensures patients understand their out-of-pocket costs before starting procedures.

-

Collections: Clear communication and documentation reduce payment disputes and improve front desk efficiency.

-

Claims Accuracy: Ensuring these figures are correct supports smoother claims submission and reduces denials.

When teams understand these interactions, it strengthens overall reimbursement predictability. Partnering with Meds Dental, a leading dental billing company, can help optimize claim submission and follow-up for maximum reimbursement while reducing administrative burden.

Do Co-Pays Count Toward Your Deductible? What You Should Know

In most insurance plans, co-pays are separate from deductibles. Payments collected for routine visits or preventive services usually do not reduce the annual deductible, meaning they are additional amounts to be tracked for patient responsibility.

For example, a $15 co-pay for a cleaning is typically not applied toward the deductible for a later restorative procedure like a root canal. This distinction is important for accurate treatment estimates and insurance claim planning.

Some plans treat co-pays differently, which is why it’s critical to review the patient’s benefit details before submitting claims. Understanding how co-pays interact with deductibles helps streamline billing, avoid under- or over-collection, and improve cash flow predictability.

Dental Insurance Basics Often Overlooked by Practices

Beyond co-pays and deductibles, several other factors can significantly impact reimbursement and patient cost estimates. Billing teams should routinely verify and account for:

-

Premiums: Monthly payments affecting overall patient costs but not directly tied to individual claims.

-

Annual Maximums: The total coverage limit per benefit year; exceeding this limit shifts all additional costs to the patient.

-

Waiting Periods: Time frames before coverage for certain procedures begins, which may delay reimbursement.

-

Provider Networks: In-network restrictions can affect claim approvals and reimbursement rates.

-

Frequency Limits: Rules that restrict how often specific treatments (e.g., cleanings or X-rays) are covered.

-

Exclusions: Services, often cosmetic, that insurance will not cover.

-

Separate Deductibles: Individual vs. family deductibles that may apply differently and impact claim calculations.

Failing to verify these plan details can result in unexpected patient balances or denied claims, even when co-pays and deductibles are correctly applied. Structured verification and documentation help ensure accurate billing, smooth insurance submissions, and higher reimbursement reliability.

Balancing Premiums and Deductibles: Optimizing Coverage Estimates

When evaluating dental insurance plans, understanding the relationship between monthly premiums and annual deductibles is critical for accurate treatment estimates and patient cost discussions. This knowledge allows providers and billing teams to anticipate out-of-pocket expenses and manage reimbursement workflows more effectively.

Key Considerations for Providers

-

Lower Premiums, Higher Deductibles: Plans with lower monthly premiums often require patients to pay more upfront before insurance coverage begins. This can impact collection timing and may require additional documentation to prevent claim delays.

-

Higher Premiums, Lower Deductibles: Plans with higher premiums usually reduce the deductible threshold, allowing coverage to begin sooner. This can accelerate claim reimbursement but may require careful verification to ensure payments align with policy limits.

Comparison of two plan types to illustrate how deductible levels influence billing workflow and patient estimates:

|

Plan Type |

Monthly Premium |

Annual Deductible |

Billing Implication |

|

Plan A |

$50 |

$5,000 |

Higher patient responsibility upfront; collect accurate estimates for major procedures. |

|

Plan B |

$100 |

$1,000 |

Deductible met faster; co-pay and coinsurance collection remains essential. |

How This Impacts Practice Workflow

Understanding these plan structures helps providers:

-

Generate precise patient estimates for major procedures.

-

Predict timing of insurance payments to avoid cash flow gaps.

-

Optimize scheduling for cost-sensitive treatments, such as coordinating restorative work after a deductible is met.

How Preventive Care Impacts Coverage and Reimbursement

Preventive services play a key role not only in patient oral health but also in revenue management and insurance claim efficiency. Understanding how preventive care interacts with co-pays, deductibles, and plan coverage allows providers to optimize billing, maximize reimbursements, and improve patient satisfaction.

-

Full Coverage for Preventive Services: Most dental plans cover routine exams, cleanings, and basic X-rays without requiring the patient to meet their deductible. This ensures predictable collections for the provider’s office while promoting regular care.

-

Early Detection Reduces High-Cost Claims: Proactively delivering preventive services can identify issues before they require complex restorative procedures, reducing the likelihood of delayed or denied claims later.

-

Patient Education and Communication: Clear explanations of preventive coverage help patients understand which services are fully covered versus those subject to co-pays or deductibles. This minimizes billing confusion and improves front-desk collection accuracy.

Workflow Benefits

-

Streamlined Claims Submission: Preventive care often bypasses deductible requirements, simplifying coding and claims review.

-

Consistent Revenue Streams: Predictable co-pay collections for preventive visits stabilize cash flow.

-

Enhanced Insurance Verification: Incorporating preventive care details into pre-visit benefit checks ensures accurate patient estimates and reduces claim resubmissions.

Co-Pays vs. Deductibles in Family and Individual Plans: What Providers Should Know

Insurance structures can differ significantly between individual and family plans, which directly impacts billing workflows, patient estimates, and claim submissions. Providers and billing teams must understand these differences to accurately calculate patient responsibility and avoid confusion at the point of care.

Family Plans

Family plans typically feature both individual and family deductibles. Once either threshold is met, coverage levels for the entire family adjust.

-

Implication for billing: If one family member undergoes a high-cost procedure, reaching the family's deductible can reduce out-of-pocket costs for other members.

-

Revenue cycle consideration: Billing teams should track which portions of the deductible have been met across family members to provide accurate pre-visit estimates and prevent under-collection.

Individual Plans

Individual plans focus solely on a single patient’s coverage and deductible.

-

Implication for billing: Each patient’s deductible and co-pay responsibility must be tracked independently.

-

Revenue cycle consideration: While simpler than family plans, providers must ensure claims and co-pay collections are calculated correctly for each patient.

Co-Pays, Deductibles, and Key Details Often Overlooked

Every insurance plan includes fine print that can impact claim reimbursement, patient billing, and overall revenue management. While some terms are straightforward, others can affect collections and estimates if not monitored carefully.

Critical Plan Elements

-

Timing of Co-Pays: Understand whether co-pays apply before or after the deductible is met to ensure accurate financial estimates.

-

Coinsurance Rules: Rates can vary for in-network versus out-of-network services, influencing patient responsibility and expected reimbursement.

-

Preventive Care Limits: Some plans cover unlimited cleanings and exams, while others impose annual caps. Knowing these limits helps schedule and bill preventive services efficiently.

-

Exclusions and Limitations: Certain procedures, such as cosmetic treatments, may not be covered. Verifying coverage prevents denials or unexpected patient balances.

-

Annual Maximums: Recognize the total yearly coverage allowed. Once exceeded, the patient becomes fully responsible, affecting collections and financial planning.

Even minor details in these plan elements can lead to significant revenue gaps if overlooked. Using structured verification and documentation ensures claims are accurate, estimates are clear, and reimbursement is maximized.

Partnering with Meds Dental provides support in tracking these details, improving claim accuracy, and streamlining financial workflows.

Smarter Choices to Keep Costs Manageable

Even with insurance coverage, out-of-pocket expenses can add up if benefits aren’t managed carefully. Taking a strategic approach helps improve patient satisfaction, streamline billing, and optimize reimbursement.

Key Strategies

-

Leverage Preventive Care: Schedule cleanings, exams, and X-rays early in the year to take advantage of full coverage and avoid hitting deductibles unexpectedly.

-

Time Major Procedures Strategically: Coordinating treatments, such as crowns or root canals, after the deductible is met ensures maximum coverage and predictable collections.

-

Verify Benefits in Advance: Check co-pays, deductibles, coinsurance, and annual maximums before treatment to set clear expectations for patients.

-

Communicate Clearly: Provide detailed estimates that break down patient responsibility, helping avoid confusion or disputes at payment time.

-

Monitor Plan Updates: Keep track of changes to coinsurance rates, annual maximums, or coverage limits to adjust estimates and billing practices proactively.

Using a structured approach reduces administrative errors, improves reimbursement predictability, and keeps financial workflows smooth. Meds Dental can assist with benefit verification, claims management, and accurate patient estimates, ensuring both insurance compliance and optimized revenue.

FAQs:

1. How should I estimate patient responsibility for co-pays and deductibles?

Use benefit verification tools to confirm plan details, including annual maximums, co-pays, deductibles, and coinsurance. This ensures accurate pre-visit estimates and reduces billing disputes.

2. Do co-pays apply before or after a deductible is met?

It depends on the insurance plan. Reviewing policy terms is essential to determine when co-pays are collected and how they affect the patient’s overall out-of-pocket cost.

3. How can I track deductible fulfillment across multiple family members?

Maintain a centralized tracking system that records individual and family deductible progress. This helps provide accurate patient estimates and prevents revenue leakage.

4. What’s the difference between co-pays, coinsurance, and deductibles from a billing perspective?

-

Co-pay: Fixed payment collected at each visit.

-

Coinsurance: Percentage of the treatment cost shared after the deductible is met.

-

Deductible: Total amount a patient must pay before the plan starts covering costs.

Accurate tracking of each ensures proper collections and reduces claim denials.

5. How can preventive care affect deductible and reimbursement planning?

Preventive services often bypass the deductible, allowing predictable collections and minimizing out-of-pocket costs for patients. Properly coding and billing preventive care ensures smooth claim approvals.

6. Can billing teams maximize reimbursement by scheduling treatments strategically?

Yes. Planning high-cost procedures after the deductible is met and coordinating preventive care can improve reimbursement efficiency and predictability.

7. How can Meds Dental support claims management for co-pays and deductibles?

Meds Dental helps verify benefits, calculate patient responsibility, manage claims, and streamline reimbursement workflows, reducing errors and improving cash flow.